Editor’s note: Seeking Alpha is proud to welcome Shashank Rai as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

SDI Productions/E+ via Getty Images

Introduction

According to the National Home Infusion Association, more than 3 million Americans rely on infusion therapy every year to receive their medications and vaccines, and the number is growing by about 12% annually. Although about 86% of this therapy is offered in the inpatient setting, the high costs associated with staying at a hospital to receive such care put pressure both on patient finances and insurance companies. For example, according to PubMed and FlexCare, the approximate per-patient cost of outpatient infusion therapy is as high as $1,000 and that for inpatient infusion therapy is $40,000. As the patient is transitioned from the hospital to home, Option Care Health (NASDAQ:OPCH), the company that we analyze in this article, provides the optimal solution for patients seeking to continue receiving their infusion therapy dosages at a low cost and with better patient satisfaction.

Option Care Health is a steadily growing safe investment that leverages a well-integrated technology infrastructure to maximize patient satisfaction while minimizing the overall cost of patient care. It targets future growth through an expansion of physician and nursing networks with a focus on chronic illness treatment and creating synergies with insurance providers. It is well-positioned within the existing ecosystem of companies to capture a larger share of the current market. It is currently at the lower end of its price range, which makes it a good stock to own for long-term value investors.

Maximizing Patient Satisfaction At A Low Cost

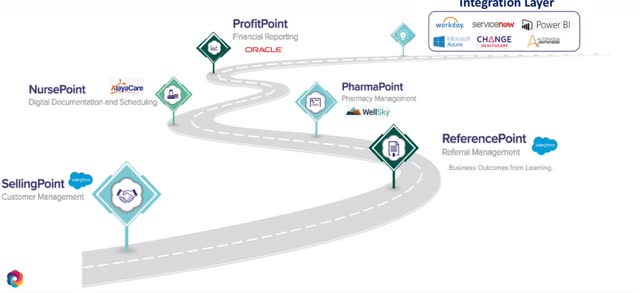

Option Care Health uses a well-integrated technology infrastructure to enhance patient care and acquire new customers. The roadmap below highlights some of the technologies providing insights into the operational efficiencies. Customer management and referral management is done using Salesforce’s (CRM) industry-leading SellingPoint and ReferencePoint technologies. For scheduling of nurse visits, AlayaCare, a venture backed firm based in Canada, is used to help optimize operations, deliver patient care, and improve patient experience. For administering prescriptions, WellSky’s PharmaPoint platform is used to prevent backlogs, obtain competitive pricing, and interface directly with providers to update prescriptions. Lastly, an integration layer powered by several technologies, such as Oracle (ORCL) ProfitPoint, Microsoft (MSFT) Azure, and Workday (WDAY), handle financial reporting, HR, and other business functions.

OPCH Investor Presentation

This technology integration allows Option Care Health to add new pharmacies, nurses, and patients seamlessly. From acquiring new customers and servicing existing customers to managing nurses and prescriptions, OPCH has sytematized the process to enhance patient experience.

Competitive Landscape And Growth Strategy

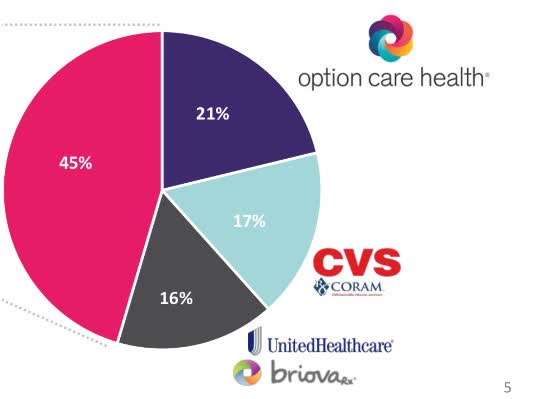

Based on OPCH investor presentation, competitors to Option Care Health are CVS Health (CVS) and UnitedHealth Group (UNH).

CVS acquired Coram in 2014 to grow its infusion therapy business. The estimated revenues from Coram in 2014 were $1.4 billion, while Option Care Health’s actual revenues were $982 billion. Even after being integrated into a larger company, Coram through CVS has been unable to drive Option Care Health out being the dominant player in infusion therapy space and it has also been unable to capture a significant share of the total market, 45% of which still belongs to more than 800+ smaller companies.

UnitedHealth Group’s strategy in the infusion therapy space has been to buy smaller companies that operate locally and regionally through its subsidiary Briovarx, which acquired Equinox Healthcare in 2013, Arc Infusion and Advanced Care in 2014, and Ambient Healthcare in 2015. With this strategy, UnitedHealth Group has only been able to amass about 16% of the total addressable market (TAM).

OPCH Investor Presentation Competitors Pie Chart

Whereas CVS’s strategy is to buy a dominant player and grow it internally and UnitedHealth Group’s strategy is to acquire smaller companies, Option Care Health’s strategy offers the best of both worlds. Instead of purchasing entire companies like UnitedHealth Group, it prefers to purchase networks that are synergistic with its business. For example, in April 2022, it announced the acquisition of Specialty Pharmacy Nursing Network Inc., which has expanded the nursing staff of Option Care Health to 2,900 across all operating regions. Such selectivity to acquisitions indicates a targeted growth strategy and disciplined investment process that streamlines integration into Option Care Health’s existing technology infrastructure, discussed earlier. And similar to CVS, Option Care Health is focused on organic growth by transforming patient experience, collaborating with payers, and leveraging commercial competitive advantages. This optimal mix of strategies is allowing Option Care Health to outcompete both CVS and UnitedHealth Group in the infusion therapy niche.

Lastly, comparing the Market Capitalization of OPCH, UNH, and CVS, we note they are $5.39 Bn, $478 Bn, and $126 Bn, respectively. Any business improvements that lead to increases in revenues, earnings, and dividends due to operational enhancements are likely to affect the share price of OPCH more than its competitors because of its smaller size. This makes OPCH also ideal for growth investors. Additionally, these stocks all trade on relatively similar price to earnings ratios, with OPCH being at a slight premium at 29.66. This indicates that the market recognizes the niche and values the earnings of OPCH.

Competitors comparison for OPCH

Option Care Health – Current Financials

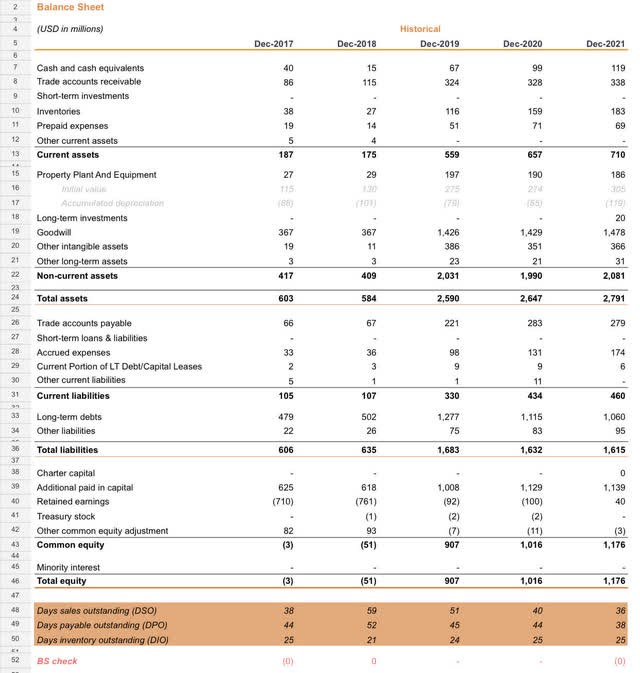

Based on the financial statements, Option Care Health has tripled its free cash from $40 million to $119 million. The total assets for the company have increased more than 4 times from $603 million to $2.8 billion. The total shareholder equity reached an inflection point in 2019, turning from negative to nearly $1 billion. Based on these figures, it is easy to see that the balance sheet has strengthened considerably.

OPCH Balance Sheet prior 5 years

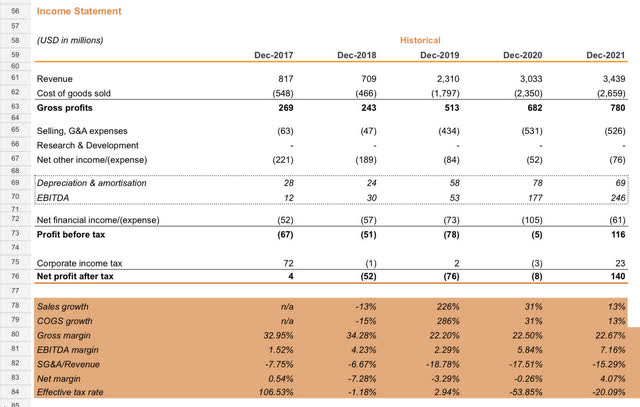

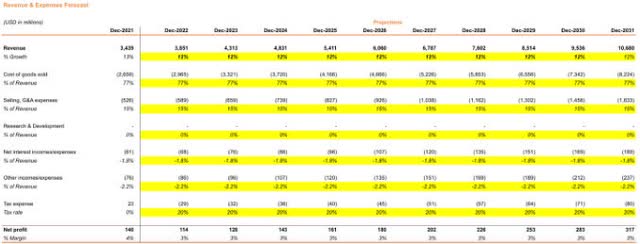

Looking at the income statement, the revenues have quadrupled from $817 million to $3.4 billion. OPCH has also steadily lowered its expenses as a percent of the revenue to increase the EBITDA around 2000% from $12 million to $246 million. With some additional financial burdens resolved, in December 2021, OPCH posted a 35 times higher profit than 2017, going from $4 million to $140 million. OPCH has also been taking advantage of tax-loss carry-forward. It’s effective tax rate has been negative. All of these factors point to a strong company with a high profit-generating potential for shareholders.

OPCH income statement past 5 years

OPCH Valuation

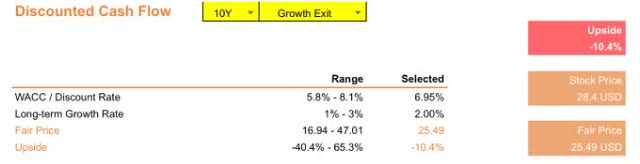

On the low end of the growth spectrum, we would anticipate Option Care Health to grow at the rate of 12% per year, which corresponds to the annual rate of increase in infusion therapy discussed earlier. We can assume that Option Care Health maintains the same overall market share, although we know that OPCH has aggressive plans to go after the chronic infusion therapy market. Additionally, we will assume a fixed percentage for the cost of goods sold, even though we know that with the highly integrated technology infrastructure, this will likely be lower over time. Using the discounted cash flow (DCF) valuation methodology over 10 years, the fair price for OPCH is $25.49, which is only around $3 below the current price of $28.4. Therefore, the market is currently valuing this company very conservatively.

Low case OPCH fair value price

Low case fair value assumptions

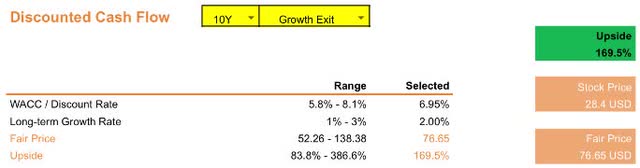

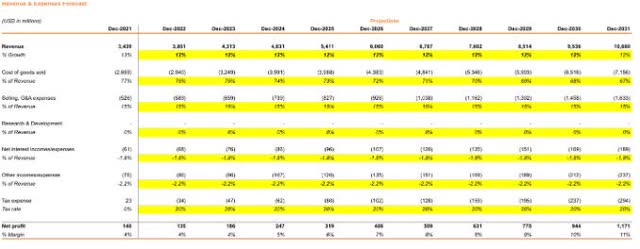

Through greater technology integrations, we can expect OPCH to lower its cost of goods sold to historical levels – around 67% over the next 10 years. With this latter scenario, we can see that OPCH’s fair value price should be 169% higher at $76.65.

High case OPCH fair value price

High case OPCH fair value assumptions

Therefore the overall reward to risk ratio for this investment is around 16 to 1 – around $3 downside to around $48 upside.

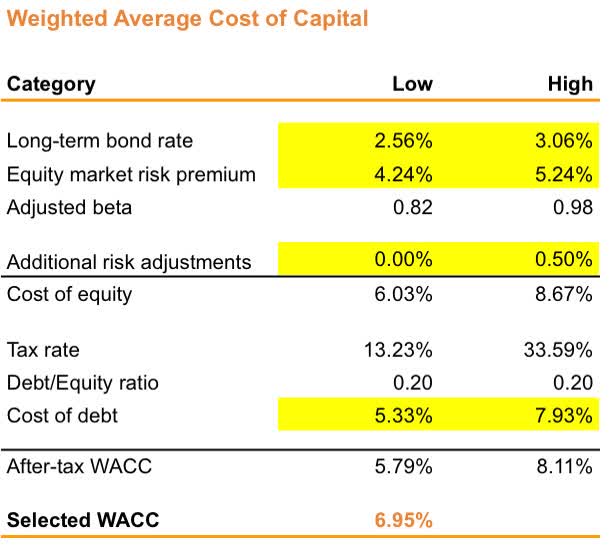

The weighted average cost of capital was selected based on the average of the high and low to factor in any potential changes to the interest rates.

OPCH Weighted Average Cost of Capital

Investment Risks

It is interesting to note that OPCH participates in infusion therapy, which is generally administered in hospitals. So a large percentage of the organic growth in infusion therapy will likely be in the inpatient setting. Therefore, OPCH is relegated to growing patients within an existing ecosystem and outcompeting CVS, UNH, and smaller competitors. This poses a challenge because patients may be relatively inflexible to switching their service providers, nurses, pharmacies, etc. Moreover, with high rates of nurses attrition reported post-COVID-19 by McKinsey, the impact of their recent acquisition of Specialty Pharmacy Nursing Network Inc would be a lot lower if the same trend continues. With a lack of adequate service, OPCH growth may stagnate.

Conclusion

For long-term investors, looking to diversify their portfolios with a steady growth stock, OPCH is a good investment to consider. It’s a relatively small company, has a disciplined growth strategy, and currently trades at the low end of its price range. All these aspects point to a great value stock poised for growth in a value-investing portfolio.

More Stories

Anxiety or Heart Disease?

Coronavirus Anxiety

All You Need To Know About Organic Natural Anti-Aging Wrinkle Cream Around The World